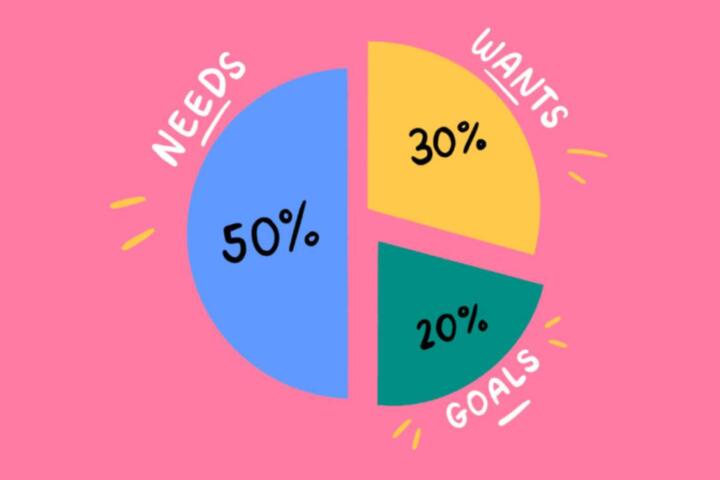

The 50/30/20 Rule

The 50/30/20 rule is a budgeting framework that splits your after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It gained traction from Senator Elizabeth Warren’s 2005 book, yet many miss how its simplicity masks real-life complexity.

Needs cover rent, groceries, utilities, and minimum loan payments—essentials you can't skip. Wants refer to dining out, entertainment, shopping, and vacations. Savings include contributions to retirement funds, emergency savings, and extra loan repayments.

Consider you take home $4,000 monthly: $2,000 toward needs, $1,200 for wants, $800 saved or used for debt. Simple, but also highly dependent on your location and personal circumstances. For example, residents in Seattle or Manhattan often find 50% for needs unrealistic due to rent hikes.

In 2023, the Bureau of Labor Statistics found the average U.S. household spends 33% on housing alone. Location matters greatly.

Common Budget Issues

Many try to force this split without adjusting for individual realities. The 50% category can balloon in high cost-of-living areas, crashing the model. They also lump all debts into savings, which can mislead prioritization.

Ignoring emergencies is another pitfall. Those dipping into the 30% want bucket to cover unexpected costs might derail savings plans. Additionally, some underestimate how lifestyle inflation wrecks the 'wants' category—they end up spending more than intended.

Consequences include growing debt, inadequate savings, or lifestyle stagnation. For example, a family juggling childcare expenses might mislabel needs and wants, causing the entire budget to skew.

Practical Steps

Assess Your Exact Income

Start with your take-home pay after taxes and mandatory deductions. Don’t use gross income; that misguides budgeting efforts. Use bank statements or payroll slips to verify. Grab a tool like Mint (version 2024.3.1) for tracking.

Define Needs Thoroughly

Be rigorous about what qualifies. Include health insurance, minimum credit payments, utilities, childcare, and groceries constrained to basics. If your rent exceeds 50%, adjust by trimming wants first. It frees you for essentials without financial guilt.

Separate Wants From Lifestyle Inflation

Track non-essentials monthly. Subscriptions, tech gadgets, eating out. That gym membership you hardly use counts as a want. Keep tabs. Tools like You Need a Budget help categorize automatically after 2 weeks of use, revealing surprises.

Prioritize Debt Payments in Savings

Pay off high-interest loans aggressively. The 20% covers this and emergency funds. For example, credit card debt over 15% APR demands quickest attention over slow retirement contributions. Once cleared, redirect funds to savings. Consistency beats occasional splurges.

Build an Emergency Fund Fast

A minimum of three months’ expenses in accessible cash. It prevents raids on the wants budget during crises. Use an online savings account like Ally for 3% APY, keeping the money liquid and growing—no penalty for quick access.

Adjust Periodically

Your budget isn’t a year-long fixed plan. Review it bi-monthly. Especially if income fluctuates or major expenses hit. Adjust the rule flexibly, leaning into savings when possible. Software that syncs your bank feeds, such as Quicken Deluxe, eases this task.

Account for Tax Variations

Tax filing status, deductions, and tax credits affect net income and thus the 50/30/20 split. If you expect a tax bill or refund, plan accordingly to avoid surprises affecting monthly budgets.

Embrace Non-Monetary Wants

Not all wants cost money—consider yoga at home or free local events. They sidestep spending but fulfill the 'wants' psychological need, stopping boredom without budget creep.

Use Real Data for Benchmarks

Analyze your expenses using past three months of bank records before setting targets. This avoids guesswork which, frankly, most people skip or misapply by relying on rules of thumb.

Real-World Examples

A freelance designer earning $5,000 monthly followed 50/30/20 initially but faced rent eating 60%. She cut wants from 30% to 15%, boosted savings to 35%, clearing $12,000 credit card debt in 8 months and easing stress.

Conversely, a young software engineer in Austin allocated 45% to needs, 35% to wants, 20% savings. His active social life and dining out pushed wants up, but he kept debt minimal. Savings grew steadily in a high-interest online account.

Both adapted the rule to fit real expenses rather than forcing the percentages rigidly. Results: lowered stress, clearer goals, improved credit scores by 40 points for the designer in short time.

Budget Comparison

| Aspect | 50/30/20 | Zero-Based | Envelope |

|---|---|---|---|

| Ease of Use | High | Medium | Low |

| Flexibility | Low | High | Medium |

| Debt Focus | Moderate | High | Low |

| Tracking Required | Minimal | High | High |

Common Mistakes

Overestimating income by ignoring tax creates budget holes. Keep net numbers in reach for accuracy.

Confusing wants with needs inflates the monthly spend cap, usually with subscriptions or dining out disguised as ""essential relaxation."" Track for 30 days, you’ll see rogue expenses.

Setting and forgetting budgets causes failure. Budgets must breathe with income changes. Miss this, and surprises—like a $400 unexpected car repair—will hit hard.

Ignoring small recurring debts is another trap; those $15 and $10 monthly charges add up fast and disrupt the 20% saving target.

Finally, relying solely on the 50/30/20 without emergency adjustments invites setbacks. Emergencies must get their own space, even if it dents wants briefly.

FAQ

Is the 50/30/20 rule good for freelancers?

Yes, but freelancers should average their income over several months to smooth out fluctuations before applying the rule.

Can I save more than 20% with this method?

Definitely. If your needs consume less than 50% and wants are minimal, you can easily push savings above 20%, speeding debt payoff or investment goals.

What if my needs cost more than 50%?

You’ll need to cut wants or increase income. The rule adapts but doesn’t excuse overspending on essentials like housing or insurance.

How does inflation affect this rule?

Inflation squeezes the needs and wants categories, meaning budgets require frequent updates to keep pace with rising costs.

Are investments covered in the 20% savings?

Yes, both emergency funds and retirement contributions count. Prioritize high-interest debt first, then channel leftover to investments.

Author's Insight

In my years refining budgets for clients, I’ve seen the 50/30/20 rule used both as a starting guide and misunderstood as a rigid formula. It helped people create financial clarity quickly. Yet many fail because they refuse to adjust percentages when their reality shifts.

Occasionally, I recommend ditching the idea of fixed percentages when income is volatile—seen this with contractors who get paid irregularly.

Even so, it forces a conversation about priorities—needs versus wants which most never track carefully. Keep tabs monthly; it pays off.

Summary

The 50/30/20 rule works best when seen as flexible guidance, not law. Start with accurate income, split cautiously, and revise often. Focus aggressively on eradicating high-interest debt within the savings portion. Adjust wants downward instead of needs when budget strain appears.

Use real expense data and monitoring tools to gauge progress. Avoid common errors like ignoring taxes or confusing spending categories. This less-hyped understanding will keep your financial health in check without stress.